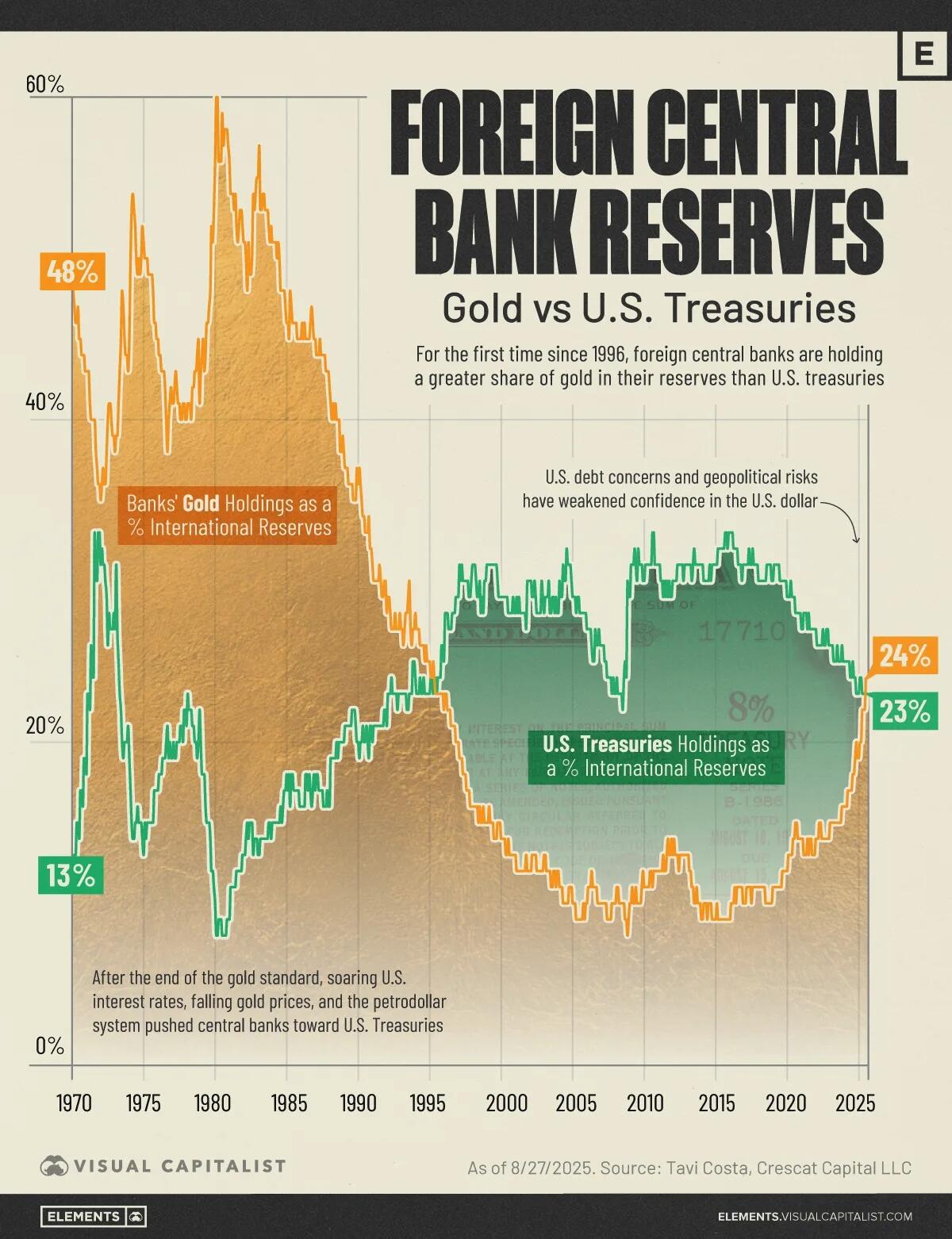

Central Banks Now Hold More Gold Than US Treasuries

Central banks have crossed a symbolic line: their combined gold reserves now exceed their U.S. Treasury holdings for the first time in nearly three decades.

The crossover underscores a gradual diversification away from dollar-denominated securities and toward hard assets.

This visualization, via Visual Capitalist’s Bruno Venditti, tracks how these shares have evolved from the 1970s to today.

{kind=link}

The data comes from Crescat Capital macro strategist Tavi Costa.

From Petrodollars to De-Dollarization

After the end of Bretton Woods, soaring real interest rates and the rise of the petrodollar steered reserve managers toward U.S. Treasuries through the 1980s and 1990s.

In the 2000s, the dollar’s depth and liquidity reinforced that preference. Since 2022, however, heavy official gold buying has picked up again — 1,136 tonnes in 2022, a record — with 2023 and 2024 maintaining historically strong accumulation. The trend is even more striking considering that nearly one-fifth of all the gold ever mined is now held by central banks.

Date

Gold Holdings As a % International Reserves

U.S. Treasuries Holdings As a % International Reserves

1/30/1970

48%

13%

1/29/1971

43%

23%

1/31/1972

36%

32%

1/31/1973

39%

31%

1/31/1974

50%

17%

1/31/1975

50%

15%

1/30/1976

44%

18%

1/31/1977

41%

20%

1/31/1978

41%

23%

1/31/1979

44%

18%

1/31/1980

60%

8%

1/30/1981

54%

11%

1/29/1982

51%

13%

1/31/1983

57%

13%

1/31/1984

51%

15%

1/31/1985

46%

17%

1/31/1986

46%

16%

1/30/1987

44%

18%

1/29/1988

41%

19%

1/31/1989

37%

21%

1/31/1990

37%

19%

2/28/1990

36%

20%

1/31/1991

30%

21%

1/31/1992

29%

23%

1/29/1993

27%

23%

1/31/1994

27%

23%

1/31/1995

24%

24%

1/31/1996

23%

28%

1/31/1997

19%

31%

1/30/1998

16%

31%

1/29/1999

15%

31%

1/31/2000

14%

29%

2/29/2000

14%

29%

3/31/2000

14%

29%

4/28/2000

13%

29%

5/31/2000

13%

29%

6/30/2000

14%

28%

7/31/2000

13%

28%

8/31/2000

13%

28%

9/29/2000

13%

28%

10/31/2000

13%

29%

11/30/2000

13%

28%

12/29/2000

13%

28%

1/31/2001

12%

29%

2/28/2001

12%

28%

3/30/2001

12%

29%

4/30/2001

12%

28%

5/31/2001

12%

28%

6/29/2001

12%

28%

7/31/2001

12%

28%

8/31/2001

12%

28%

9/28/2001

13%

27%

10/31/2001

12%

30%

11/30/2001

12%

30%

12/31/2001

12%

30%

1/31/2002

12%

30%

2/28/2002

13%

29%

3/29/2002

13%

29%

4/30/2002

13%

30%

5/31/2002

13%

29%

6/28/2002

12%

28%

7/31/2002

12%

28%

8/30/2002

12%

28%

9/30/2002

12%

28%

10/31/2002

12%

30%

11/29/2002

12%

29%

12/31/2002

13%

28%

1/31/2003

13%

29%

2/28/2003

12%

29%

3/31/2003

12%

29%

4/30/2003

12%

30%

5/30/2003

12%

28%

6/30/2003

11%

28%

7/31/2003

11%

29%

8/29/2003

12%

29%

9/30/2003

12%

28%

10/31/2003

11%

29%

11/28/2003

12%

28%

12/31/2003

12%

28%

1/30/2004

11%

30%

2/27/2004

11%

29%

3/31/2004

11%

29%

4/30/2004

10%

31%

5/31/2004

10%

30%

6/30/2004

10%

30%

7/30/2004

10%

32%

8/31/2004

10%

31%

9/30/2004

11%

31%

10/29/2004

11%

31%

11/30/2004

11%

30%

12/31/2004

10%

29%

1/31/2005

10%

29%

2/28/2005

10%

29%

3/31/2005

9%

28%

4/29/2005

9%

29%

5/31/2005

9%

29%

6/30/2005

9%

28%

7/29/2005

9%

28%

8/31/2005

9%

28%

9/30/2005

10%

28%

10/31/2005

9%

28%

11/30/2005

10%

28%

12/30/2005

10%

27%

1/31/2006

11%

27%

2/28/2006

11%

27%

3/31/2006

11%

27%

4/28/2006

12%

26%

5/31/2006

11%

25%

6/30/2006

11%

25%

7/31/2006

11%

27%

8/31/2006

11%

26%

9/29/2006

10%

26%

10/31/2006

10%

27%

11/30/2006

10%

26%

12/29/2006

10%

26%

1/31/2007

10%

26%

2/28/2007

10%

26%

3/30/2007

10%

25%

4/30/2007

10%

25%

5/31/2007

9%

24%

6/29/2007

9%

24%

7/31/2007

9%

24%

8/31/2007

9%

24%

9/28/2007

10%

23%

10/31/2007

10%

24%

11/30/2007

10%

23%

12/31/2007

10%

23%

1/31/2008

11%

24%

2/29/2008

11%

23%

3/31/2008

10%

23%

4/30/2008

10%

23%

5/30/2008

10%

23%

6/30/2008

10%

22%

7/31/2008

10%

24%

8/29/2008

9%

25%

9/30/2008

9%

24%

10/31/2008

8%

30%

11/28/2008

9%

29%

12/31/2008

10%

29%

1/30/2009

10%

31%

2/27/2009

11%

31%

3/31/2009

10%

31%

4/30/2009

10%

32%

5/29/2009

11%

31%

6/30/2009

10%

30%

7/31/2009

10%

32%

8/31/2009

10%

31%

9/30/2009

10%

31%

10/30/2009

11%

31%

11/30/2009

12%

30%

12/31/2009

11%

30%

1/29/2010

11%

31%

2/26/2010

11%

31%

3/31/2010

11%

31%

4/30/2010

11%

31%

5/31/2010

12%

31%

6/30/2010

12%

31%

7/30/2010

11%

33%

8/31/2010

12%

33%

9/30/2010

12%

31%

10/29/2010

12%

31%

11/30/2010

12%

31%

12/31/2010

12%

31%

1/31/2011

12%

31%

2/28/2011

12%

30%

3/31/2011

12%

30%

4/29/2011

13%

29%

5/31/2011

12%

30%

6/30/2011

12%

29%

7/29/2011

13%

30%

8/31/2011

14%

29%

9/30/2011

13%

30%

10/31/2011

13%

29%

11/30/2011

14%

29%

12/30/2011

13%

30%

1/31/2012

14%

30%

2/29/2012

13%

30%

3/30/2012

13%

30%

4/30/2012

13%

31%

5/31/2012

12%

31%

6/29/2012

13%

31%

7/31/2012

13%

31%

8/31/2012

13%

31%

9/28/2012

13%

30%

10/31/2012

13%

31%

11/30/2012

13%

31%

12/31/2012

13%

31%

1/31/2013

13%

31%

2/28/2013

12%

31%

3/29/2013

12%

31%

4/30/2013

11%

30%

5/31/2013

11%

31%

6/28/2013

10%

32%

7/31/2013

10%

31%

8/30/2013

11%

31%

9/30/2013

10%

31%

10/31/2013

10%

31%

11/29/2013

10%

31%

12/31/2013

9%

31%

1/31/2014

9%

31%

2/28/2014

10%

30%

3/31/2014

10%

30%

4/30/2014

10%

30%

5/30/2014

9%

30%

6/30/2014

10%

30%

7/31/2014

10%

31%

8/29/2014

10%

30%

9/30/2014

9%

31%

10/31/2014

9%

31%

11/28/2014

9%

31%

12/31/2014

9%

31%

1/30/2015

10%

31%

2/27/2015

9%

32%

3/31/2015

9%

32%

4/30/2015

9%

32%

5/29/2015

9%

32%

6/30/2015

9%

32%

7/31/2015

9%

32%

8/31/2015

9%

33%

9/30/2015

9%

33%

10/30/2015

9%

32%

11/30/2015

9%

33%

12/31/2015

9%

33%

1/29/2016

10%

33%

2/29/2016

10%

33%

3/31/2016

10%

32%

4/29/2016

11%

32%

5/31/2016

10%

32%

6/30/2016

11%

32%

7/29/2016

11%

31%

8/31/2016

11%

31%

9/30/2016

11%

31%

10/31/2016

11%

30%

11/30/2016

10%

31%

12/30/2016

10%

31%

1/31/2017

10%

31%

2/28/2017

11%

31%

3/31/2017

11%

31%

4/28/2017

11%

32%

5/31/2017

11%

31%

6/30/2017

10%

31%

7/31/2017

11%

32%

8/31/2017

11%

31%

9/29/2017

11%

31%

10/31/2017

11%

31%

11/30/2017

11%

31%

12/29/2017

11%

30%

1/31/2018

11%

30%

2/28/2018

11%

30%

3/30/2018

11%

30%

4/30/2018

11%

30%

5/31/2018

11%

30%

6/29/2018

10%

30%

7/31/2018

10%

31%

8/31/2018

10%

31%

9/28/2018

10%

31%

10/31/2018

10%

31%

11/30/2018

10%

30%

12/31/2018

11%

30%

1/31/2019

11%

31%

2/28/2019

11%

31%

3/29/2019

11%

31%

4/30/2019

11%

31%

5/31/2019

11%

31%

6/28/2019

11%

30%

7/31/2019

11%

30%

8/30/2019

12%

30%

9/30/2019

12%

30%

10/31/2019

12%

30%

11/29/2019

12%

30%

12/31/2019

12%

29%

1/31/2020

13%

29%

2/28/2020

13%

29%

3/31/2020

13%

30%

4/30/2020

13%

29%

5/29/2020

14%

29%

6/30/2020

14%

29%

7/31/2020

15%

28%

8/31/2020

15%

28%

9/30/2020

14%

28%

10/30/2020

14%

28%

11/30/2020

14%

28%

12/31/2020

14%

27%

1/29/2021

14%

27%

2/26/2021

13%

28%

3/31/2021

13%

28%

4/30/2021

13%

28%

5/31/2021

14%

27%

6/30/2021

13%

28%

7/30/2021

14%

27%

8/31/2021

14%

27%

9/30/2021

13%

27%

10/29/2021

13%

27%

11/30/2021

13%

27%

12/31/2021

14%

27%

1/31/2022

14%

26%

2/28/2022

14%

26%

3/31/2022

15%

26%

4/29/2022

15%

26%

5/31/2022

14%

26%

6/30/2022

14%

27%

7/29/2022

14%

26%

8/31/2022

14%

26%

9/30/2022

14%

27%

10/31/2022

14%

27%

11/30/2022

14%

26%

12/30/2022

15%

26%

1/31/2023

15%

26%

2/28/2023

15%

26%

3/31/2023

15%

25%

4/28/2023

15%

25%

5/31/2023

15%

25%

6/30/2023

15%

26%

7/31/2023

15%

25%

8/31/2023

15%

25%

9/29/2023

15%

25%

10/31/2023

16%

26%

11/30/2023

16%

25%

12/29/2023

16%

25%

1/31/2024

16%

25%

2/29/2024

16%

25%

3/29/2024

17%

25%

4/30/2024

17%

25%

5/31/2024

17%

24%

6/28/2024

17%

24%

7/31/2024

18%

25%

8/30/2024

18%

24%

9/30/2024

19%

24%

10/31/2024

20%

23%

11/29/2024

19%

23%

12/31/2024

19%

23%

1/31/2025

20%

24%

2/28/2025

20%

24%

3/31/2025

22%

23%

4/30/2025

22%

23%

5/30/2025

22%

23%

6/30/2025

24%

23%

As political uncertainty and geopolitical risks continue to fuel safe-haven demand, this purchasing momentum has also lifted prices: gold surpassed $4,000 an ounce for the first time ever in October 2025.

Why “More Gold than Treasuries” Matters

Crossing above Treasuries signals that reserve managers are prioritizing durability, portability, and neutrality over yield.

According to the IMF, gold’s share of global reserves climbed to about 18% in 2024, up sharply from mid-2010s levels, reflecting a structural reweighting toward tangible assets.

Seen as an alternative to heavily indebted fiat currencies, especially the U.S. dollar, the share of gold in central bank reserves has increased most among emerging market economies. China, Russia, and Türkiye have been the largest official buyers over the past decade.

If you enjoyed today’s post, check out U.S. Dollar Index Falls 10.1% in 2025, Steepest Drop in Three Decades on Voronoi, the new app from Visual Capitalist.

Tyler Durden

Fri, 10/10/2025 – 23:00

https://www.zerohedge.com/geopolitical/central-banks-now-hold-more-gold-us-treasuries